Tata Steel, State Aid and Brexit

04/04/2016

Ruth was interviewed on Radio 5 Live Breakfast show on 31 March, discussing why the Government could not give State aid to save Tata Steel, and how this might be affected if the UK were to leave the EU. This blog expands on some of the comments she made.

There is a strong public and political demand to save Tata Steel. In the short term it is unlikely that this could be done with private money, as there appear to be no imminent buyers, and so the demand is that the State step in with public funding. Nationalisation has been suggested as an option, reflecting the way the banks were rescued at the time of the financial crash. Unfortunately, this is not legal under the State aid rules.

What is State aid?

State aid means using taxpayer-funded resources to provide assistance to an economic undertaking in a way that gives it an advantage that it could not get in the open market. The State aid rules in the UK come from EU law.

Would it be against EU regulations to provide funding to Tata Steel in a time of need?

Unfortunately, yes. The fact that all the economic factors go against the UK steel industry is not relevant, nor is the potentially devastating impact on the wider local economy were it to close. The EU has already ruled on this: in January the competition commissioner ruled that the Belgian government had illegally provided €211m to steel companies in one of its depressed regions, and ordered that the money be repaid. She also announced an investigation into €2bn of similar aid given by the Italian government to support its steel industry.

The EU takes the view that State aid cannot be used if it distorts competition, and that EU regional funding is available to help with the social consequences of closing down industries that are uncompetitive.

So how come the banks were bailed out?

There is a fundamental difference between banks and steel. If the UK, or Belgian, or Italian steel industry has to shut down, then other steel companies will pick up their contracts. Such commercial competition is the thrust behind most of the legislation: saving any of the ailing companies would adversely affect the other steel providers, who would not be able to take those contracts. In the case of the banks, their mutual interdependence made that impossible. Because they had all lent to each other, the collapse of any of the banks would have led to the collapse of the whole financial system. So, saving the banks was not anti-competitive, it was in fact supporting the market economy.

Then the EU bent the rules for the banks?

No, it did not bend the rules, it used provisions in the Rescue and Restructuring Guidelines which enable State aid in certain very limited circumstances. Unfortunately, this would be difficult to apply to steel.

The ‘Rescue’ part of the R&R Guidelines is very limited, and provides that State aid can be given for a limited amount, and a limited duration (months), and is reversible. The ‘Restructuring’ part is slightly more flexible, and is what was used for the banks. However, it involves having a clear plan for return to viability, in a relatively short time (albeit years rather than months), and needs co-investment of about 50% alongside the State funds.

Neither of these forms of funding appears to be available for the steel industry in any of the EU countries, mostly because global economic conditions show no sign of changing in the foreseeable future, and without an increase in economic activity, and a decrease in Chinese steel exports[1], there is little possibility of a viable plan for recovery. And, any such plan would need significant co-investment funding, which is not really available.

R&R is probably the way in which the Scottish government has managed to fund the Dazzell and Clydebridge steel plants, as bridging finance during the sales process which was already underway. However, it will be more difficult to find a funded buyer for the Port Talbot plant, although the politicians are now actively working on finding such a solution. Without a credible and immediate buyer, this route is very unlikely.

So how did the Government manage to nationalise East Coast Rail?

When the National Express East Coast Rail franchise collapsed in 2009 the government nationalised the line (although it has since re-privatised it). This, I understand, came under an exemption to protect essential infrastructure.

Would we be able to provide State aid if we left the EU?

At first sight, you’d think that should be the case. EU law prevents State aid, so leave the EU and all will be fine. However, once you start looking at the situation, this is not the case.

The UK trades internationally, and therefore needs trading agreements with all other countries and trading blocs. At the moment, our trading agreements are done through the EU. Were we to leave the EU, we would need to implement other arrangements, so that we could carry on trading.

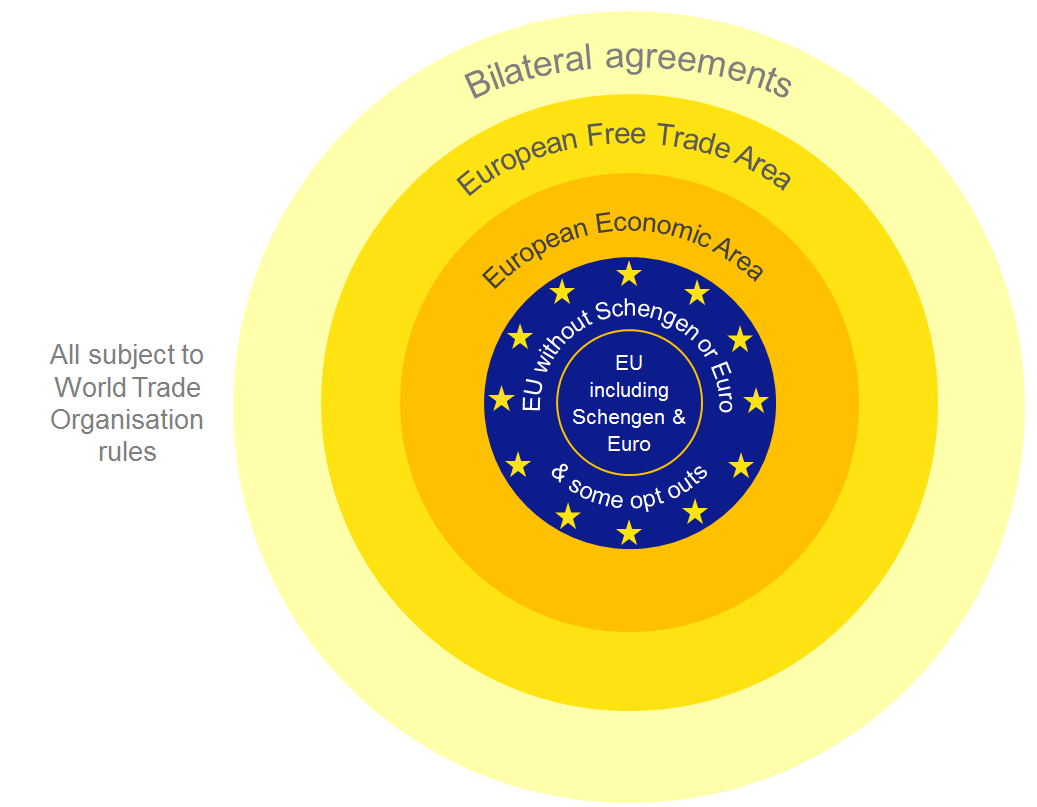

If Brexit takes place, there are various alternatives, as illustrated in the diagram below. At the centre is EU membership, and I’ve split out the core EU countries, those who signed up to Schengen, the euro and everything, from the outer circle of countries, including the UK, who have opted out of certain matters. EU regulations on State aid cover all of the countries in the blue EU circles.

One alternative for Brexit would be to emulate Norway, and join the European Economic Area (EEA). This would give us access to the EU single market, although we would still have to renegotiate trade agreements with all the non-EU countries/trading blocs. However, counties in the EEA are bound by the EU’s State aid rules, so it would not change the steel situation. (EEA countries are actually bound by a lot of the EU’s regulations, and have to pay a considerable sum into the EU budget, but that is a topic for another day.)

The next layer out is EFTA, the European Free Trade Area. This is the trading model used by Switzerland. EFTA means partial access to EU markets, and accordingly, being subject to fewer EU regulations. However, my understanding is that Switzerland still has to abide by the EU State aid regulations.

The third alternative, I’ve just called ‘bilateral agreements’. This covers a range of alternatives including, for example, customs union such as Turkey has with the EU, or the extensive agreements that Canada has concluded, after 10 years of negotiation. Bilateral agreements will mean that products sold into the EU have to comply with EU regulations, but not that countries have to adopt EU regulation more generally. So, the EU State aid rules won’t apply. However, at that point we would still be subject to the World Trade Organisation rules.

World Trade Organisation rules apply to EU countries already – for example, the WTO ruled that various subsidies given for the development of Airbus were illegal. As with the EU, the WTO’s main aim is to avoid factors that distort competitive markets. The relevant regulation goes under the title of Subsidies and Countervailing Measures, and clearly includes State rescue of ailing organisations in its definition of Subsidies.

So is that it?

I’m neither a politician nor an international lawyer, so I can’t conclude definitely. But as far as I can see, State aid to save Tata would be in contravention of both EU and WTO regulations. Were we to leave the EU, even if we didn’t join EEA or EFTA, the WTO rules would still apply, as would all the individual rules we negotiated in a myriad of bilateral agreements.

[1] Chinese steel producers have been accused of ‘dumping’, selling at artificially low prices. This is against EU and WTO regulations. Likewise, steel is a cyclical industry, and the fact that a resurgence in world demand is unlikely in the short-term future does not mean it won’t ultimately rise. However, these are not issues to deal with in this blog.

Categories & Tags:

Leave a comment on this post:

You might also like…

Building more than research: Reflections from the ECRn Symposium 2026

There’s something quietly powerful about a room full of early career researchers. Not just the ideas, although there were plenty of those—but the conversations, the curiosity, and the sense that everyone is figuring things ...

Library services over Easter, 3-6 April

Kings Norton Library will remain open for study 24/7. You will need your University ID card to enter the building and can use the self-service machines to borrow and return items as usual. Barrington Library ...

How do I access the full-text of Harvard Business Review (HBR)?

This is a frequently asked question, and it's worth knowing how to access this key management journal. So, how do you access HBR in full-text? The short answer is via our eJournals finder. You can find ...

Engineering problem to solve? Let Knovel help you find a solution

Did you know that Knovel provides you with more than just eBooks? Knovel is a key database for many engineering, mechanical and materials courses here at Cranfield University, and contains content from an extensive range ...

What happens when female scholars meet influential leaders?

On the 5 March 2026, our British Council Women in STEM Scholars had the privilege of sitting down with two excellent role models of industry and academia: Professor Dame Karen Holford, ...

From MSc to CEO: Igniting a research revolution

For many, a master’s degree is achieving a big milestone. Kilyan Ocampo, Computational Fluid Dynamics alumni shares how studying at Cranfield helped launch his career in the energy sector. Today, Kilyan ...

Thank you for concise yet extremely comprehensive summary of this issue.

So well explained. Ruth is always great with her simplicity in explaining things.

Really a very strong issue and also effect the country economy .Thanks a lot for explaining this issue very well .

explained very well with all details about the issue !

So well discussed with the all important stuff related to this