Beyond Budgeting… A journey towards real customer service – Part 2 / 2

27/07/2017

Last week, we introduced the idea of Beyond Budgeting and how it chimes with our work with Cranfield on “A Systems Approach to Project Management”. It challenges the current standard practice of setting rigid budgets on an annual (or longer term) basis and then tracking variance from budget month by month.

This may seem scary for some finance types, but there are many advantages of adopting the approach promoted by the Beyond Budgeting Institute (www.bbrt.org). Some global organisations are adopting this approach and doing very well thank you – e.g. Handelsbanken, Maersk, Lego, E&Y and many others……

So, if not tracking results and their variance from budget on a monthly basis, what’s the alternative?

The answer is to first consider if monthly is the right timeframe – surely this should be determined by the nature of the business or the world-system at hand, and any contextual changes in the markets or communities they serve. For example, retail may require daily assessment, whereas ship-building might require monthly…

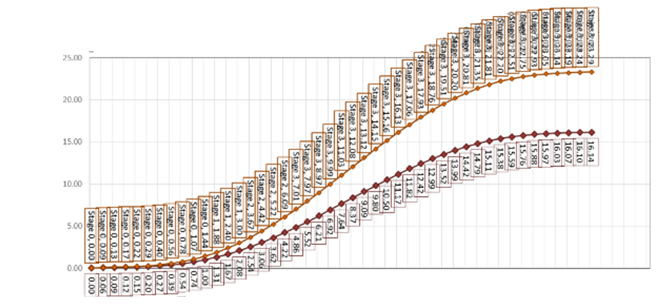

Second, can you get data about what peers are achieving, and then position your results against this group? In essence you’re creating a “reference class” of results which will give you an envelope centred around an average which you can then compare your results against. It might be projected spend over the next two years, with a “lazy S” profile. If the spend at each review period is not outside the envelope, don’t get excited!

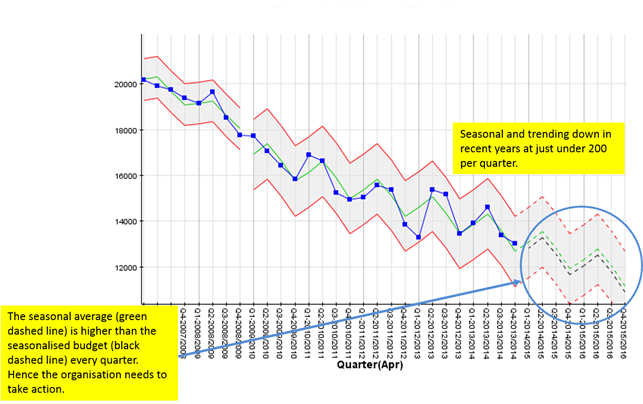

Third, and along with this, you might want to use extended-SPC techniques to track whether the patterns and trends are “in the right direction”. Below, you might be tracking costs or spend which you may be wanting to bring down by approx. 15% over the next year. By looking at your previous actual costs/spend profile up until Q4 2013/14 (the envelope between the upper and lower red guidelines), you can project this forwards (dashed lines) and superimpose the seasonalised required budget reduction (dashed black line) and look at the likelihood of achieving the reduction going forwards.

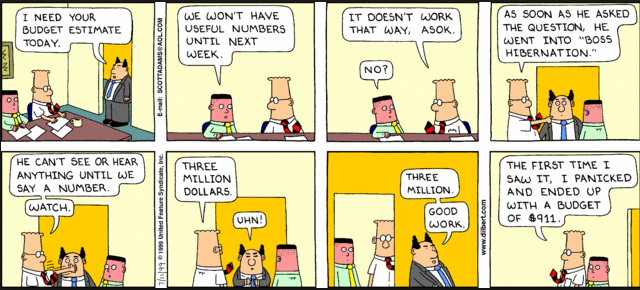

By looking at the evidence (the data) in this way, organisations become energised around what action to take to move in the right direction going forwards, rather than looking backwards and trying to justify why some result differed from some arbitrary budget set some time in the distant past. It accepts that there is something called variation in the world, beyond the precise control of any one manager. Of course, until your seniors really understands real-world variation, they may well go into “boss hibernation” (or adopt the head-in-sand approach)!

Categories & Tags:

Leave a comment on this post:

You might also like…

Using AI tools for your literature review

There are a proliferation of AI tools that can help you organise your life, work and study. This post focuses on academic or scholarly tools that have been developed to enhance the literature searching process, whether for independent research, an assignment or thesis. Bear in mind that these predominantly relate to finding journal/research papers, and not technical, business or trade sources such as standards, market research, industry reports or financial data. So ...

Finding successful past Cranfield theses

It’s always a good idea to look at examples of theses before you start work on your own. You may find them valuable for reading previous research, and for looking at structure, style and methodology. ...

On‑campus or off‑campus? How Cranfield students found their home away from home

Finding the right place to live is one of the biggest decisions you’ll make as you begin your student journey. Whether you’re looking for the convenience and community of living on-campus or the independence ...

Avoiding common referencing errors

As librarians, we get to see the full spectrum of reference lists in student work —from exemplary to … well, let’s just say, works still very much in progress! We are experts in spotting mistakes ...

Using your Mendeley library after you have left Cranfield

So you have spent the whole year (or more) lovingly collecting references around the topics that matter to you and now you have a large, personalised library in Mendeley Reference Manager containing all that information. ...

Referencing the use of generative AI in your work

We recognise that Artificial Intelligence (AI) has, and will increasingly, become a part of our everyday lives and that we need to adapt to it. Hopefully you will have already seen the guidance for staff ...