Beyond Budgeting… A journey towards real customer service – Part 2 / 2

27/07/2017

Last week, we introduced the idea of Beyond Budgeting and how it chimes with our work with Cranfield on “A Systems Approach to Project Management”. It challenges the current standard practice of setting rigid budgets on an annual (or longer term) basis and then tracking variance from budget month by month.

This may seem scary for some finance types, but there are many advantages of adopting the approach promoted by the Beyond Budgeting Institute (www.bbrt.org). Some global organisations are adopting this approach and doing very well thank you – e.g. Handelsbanken, Maersk, Lego, E&Y and many others……

So, if not tracking results and their variance from budget on a monthly basis, what’s the alternative?

The answer is to first consider if monthly is the right timeframe – surely this should be determined by the nature of the business or the world-system at hand, and any contextual changes in the markets or communities they serve. For example, retail may require daily assessment, whereas ship-building might require monthly…

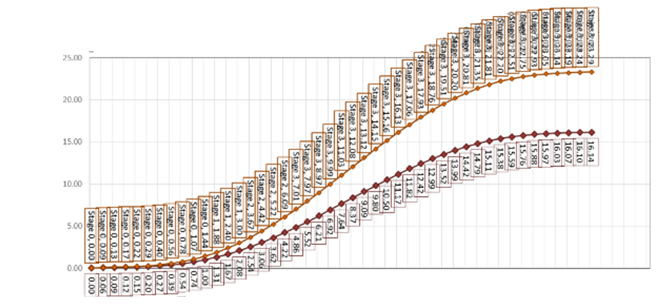

Second, can you get data about what peers are achieving, and then position your results against this group? In essence you’re creating a “reference class” of results which will give you an envelope centred around an average which you can then compare your results against. It might be projected spend over the next two years, with a “lazy S” profile. If the spend at each review period is not outside the envelope, don’t get excited!

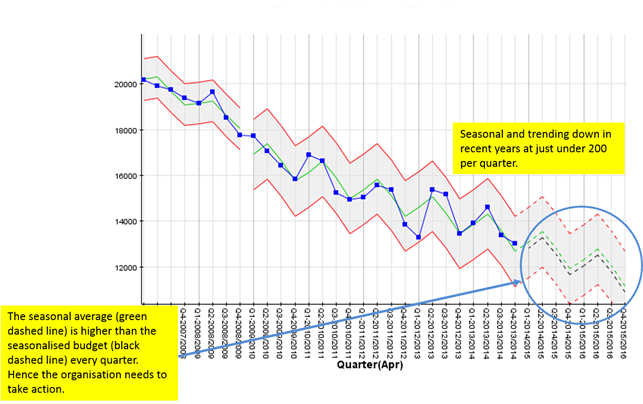

Third, and along with this, you might want to use extended-SPC techniques to track whether the patterns and trends are “in the right direction”. Below, you might be tracking costs or spend which you may be wanting to bring down by approx. 15% over the next year. By looking at your previous actual costs/spend profile up until Q4 2013/14 (the envelope between the upper and lower red guidelines), you can project this forwards (dashed lines) and superimpose the seasonalised required budget reduction (dashed black line) and look at the likelihood of achieving the reduction going forwards.

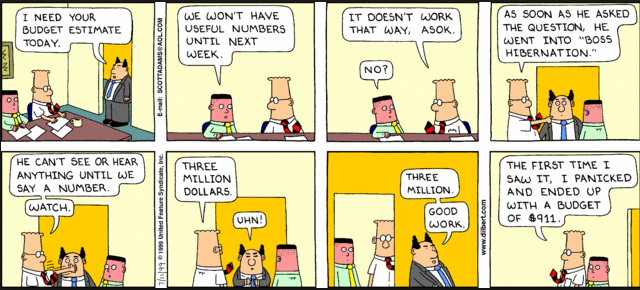

By looking at the evidence (the data) in this way, organisations become energised around what action to take to move in the right direction going forwards, rather than looking backwards and trying to justify why some result differed from some arbitrary budget set some time in the distant past. It accepts that there is something called variation in the world, beyond the precise control of any one manager. Of course, until your seniors really understands real-world variation, they may well go into “boss hibernation” (or adopt the head-in-sand approach)!

Categories & Tags:

Leave a comment on this post:

You might also like…

Getting started on your School of Management thesis

Writing a thesis, business plan, internship project or company project can be a daunting task, and you might have some uncertainty or questions around how to get started. This post will share some ideas and ...

Sustainability by royal request: Managing an event fit for a King

The Coronation of King Charles III on May 6th 2023, was watched by millions of people around the world with tens of thousands of people travelling to Central London to witness the pageantry firsthand. ...

Getting started on your Master’s thesis

Please note: This post is intended to provide advice to all students undertaking a thesis in the Schools of Aerospace, Transport and Manufacturing; Water, Energy and Environment, and Defence and Security. There is separate advice ...

Finding your tribe: “Joining the sustainability community was the best decision”

For students on Cranfield’s Sustainability Business Specialist Apprenticeship, community and camaraderie is a vital component for success. Designed in consultation with industry, the part-time Level 7 apprenticeship aims to deepen participants’ knowledge of the ...

“My sustainability studies gave me the confidence to take on Amazon”

Not everyone would have the confidence to challenge a big global power like Amazon but, for Colin Featherstone, Senior Technology Manager and Tech Sustainability Lead at Morrisons, his Cranfield studies equipped him with the ...

My Apprenticeship Journey – Broadening Horizons

Laura, Senior Systems Engineer at a leading aircraft manufacturing company, joined Cranfield on the Systems Engineering Master’s Apprenticeship after initially considering taking a year off from her role to complete an MSc. Apprenticeship over MSc? ...